I remember standing next to a family last year watching their home burn. The red and orange flames shooting up into the sky. Their faces blank with shock. In that moment, they didn’t just lose their house—they lost the Christmas ornaments from their grandma, the height marks on the kitchen wall, the photos that wasn’t backed up nowhere.

When your house burns down in Delaware, the days after are a fog. You got nowhere to sleep, nothing to wear, and a mountain of insurance paperwork waiting. Most people don’t know the first thing about what to do next.

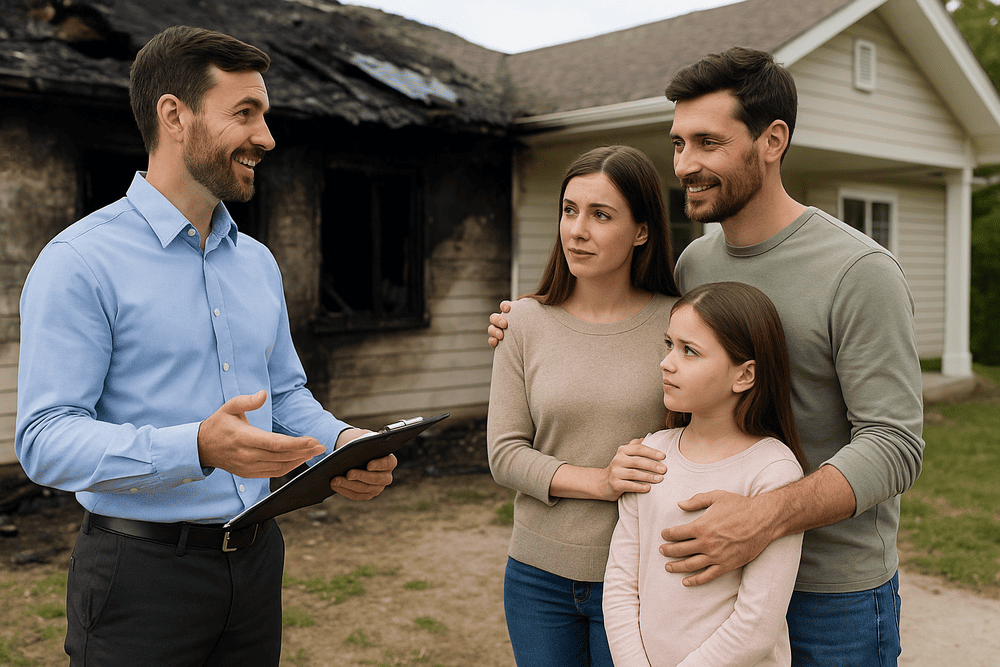

That’s where Delaware fire claims adjusters come in. We work for you, not the insurance company. Our only job is making sure you get every dollar you deserve to rebuild your life. Unlike the adjuster the insurance company sends, who’s trying to save them money, we’re fighting to maximize what you get. Call us at 302-279-2536 for immediate help.

Fire Claims Adjusters has helped hundreds of Delaware homeowners navigate the complex insurance claim process after devastating fires.

Fire claims in Delaware got certain challenges you won’t find in other states. Experienced public adjusters has handled claims in every county, from the beaches of Sussex to the suburbs of New Castle, and we know the local regulations that effect your claim.

The truth is, what you do in the days right after a fire decides how much money you’ll end up with. Make the wrong move, and you could lose thousands. I’ve seen it too many times.

In this guide, I’ll take you through exactly what you need to do after a fire destroys your Delaware home. We’ll cover how to handle your immediate needs, document what’s gone, understand what your policy actually covers (not what the insurance company tells you it covers), and how professional help can make all the difference.

Those first three days after your house burns down are when you make decisions that affect everything that comes after. Most people never been through this before and don’t realize how important these early hours are.

First thing—don’t go back in your house until officials say it’s safe. Even if the fire’s out, that don’t mean the danger is. I had a client in Dover who went back too soon and part of their ceiling came down. They was lucky to get out.

Delaware fire marshals gotta clear your property before you can safely return. This ain’t just red tape—it’s keeping you alive. Even if the structure looks okay from outside, fire damages the bones of your house in ways you can’t see. Support beams might be weakened, floors could collapse, and walls that look fine might fall over with the slightest touch.

The air inside is another problem most people don’t think about. The smoke after a fire ain’t just smoky—it’s toxic. Burning furniture, plastics, and building materials release chemicals you don’t wanna breathe. Some clients think they can just open a window and it’ll be fine, but that smoke gets everywhere and sticks around.

Here’s what you need to know about safety hazards:

For more detailed safety information, give us a call and we can explain what to watch out for.

You need a place to stay tonight, and probably for months to come. The Red Cross Delaware can help right away with emergency housing, clothes, and food. They got volunteers who respond 24/7 to fires across the state.

Delaware’s got specific housing resources you should know about. The Delaware State Housing Authority has emergency programs for fire victims. In Wilmington, there’s additional city resources that can help find temporary apartments.

Depending on the size of the fire, FEMA might get involved too. Check if your situation qualifies for federal assistance—this ain’t automatic, you gotta apply. Many Delaware homeowners don’t realize they might be eligible for this help on top of their insurance.

| Organization | What They Provide | How To Contact |

|---|---|---|

| Red Cross Delaware | Emergency housing, clothes, food | 1-800-RED-CROSS |

| Salvation Army Delaware | Emergency assistance, emotional support | 302-472-0700 |

| Delaware State Housing Authority | Temporary housing programs | 302-739-4263 |

| FEMA | Disaster assistance if qualified | 1-800-621-FEMA |

How do you make a list of everything you owned when it’s all gone? This is one of the hardest parts. Start with your smartphone—there’s apps made for this exact situation that walk you through each room of your house to help you remember what was there.

Go room by room in your mind. Start with the big stuff—furniture, electronics, appliances. Then move to smaller items. For the kitchen, think about that expensive mixer, the set of knives, all your dishes. For bedrooms, remember clothing (count how many pairs of jeans, shirts, etc.), jewelry, and electronics.

Getting other people to help verify what you owned is super important. Family members who visited your house can remind you of things. Amazon and other online shopping accounts have your purchase history. Credit card statements show big purchases. Your kids might have pictures of the inside of your house on their phones or social media.

Don’t forget to document the outside too—your grill, patio furniture, landscaping equipment, and any outbuildings like sheds. Take photos of the damage as soon as you’re allowed back on the property, before anything gets moved or cleaned up.

Documentation checklist:

Learn more about our fire damage documentation services.

That policy you paid for all these years? It’s time to actually understand what’s in it. And it ain’t written to be easy to understand.

The biggest thing you need to know is whether you got Replacement Cost or Actual Cash Value coverage. This makes a huge difference in how much money you get.

Replacement Cost means they pay what it costs to buy everything new today. Actual Cash Value means they subtract depreciation—so that 10-year-old couch might only be worth a couple hundred dollars to them, even though buying a new one costs way more.

Your policy also covers Additional Living Expenses, which pays for your hotel, apartment, or rental house while yours gets rebuilt. But there’s usually a time limit or dollar cap. I had clients in Rehoboth Beach who ran out of ALE money before their house was finished, and had to pay rent out of pocket for the last two months.

Another big deal is code upgrade coverage. Delaware building codes changed a lot in recent years. If your house was older, rebuilding it to current code can cost tens of thousands more. Some policies cover this, some don’t. If yours don’t, you gotta pay that difference yourself.

For specific questions about Delaware insurance regulations, contact our office directly.

Key policy terms to understand:

Read our detailed guide to understanding fire insurance policy coverage for more information.

Your policy covers more than just the house and stuff inside. Most Delaware policies include coverage for landscaping and other structures like fences, sheds, and detached garages. I’ve seen clients get thousands for mature trees and plantings they lost.

Many newer policies have identity theft protection built in. If important documents were destroyed in the fire and you worry about identity theft, check if this coverage is in your policy.

Did you lose all the food in your fridge and freezer? That’s covered too. Same for emergency purchases like toiletries, clothes, and food right after the fire. Keep every receipt—even that $5 you spent on a toothbrush and toothpaste.

Commonly overlooked coverage areas:

At Fire Claims Adjusters, we help homeowners identify all these hidden benefits in their policies.

Here’s where things get tricky. Most policies have caps for certain types of items. Jewelry might be limited to $1,500 total unless you bought extra coverage. Same for art, collections, and antiques. One family in Newark had a baseball card collection worth $20,000, but their policy only paid $2,500 because they didn’t have a separate rider for it.

Delaware has specific deadlines for filing paperwork after a loss. Miss these deadlines, and the insurance company can deny your claim completely. The proof of loss form is especially important—this is the official document where you list everything you lost.

When everything’s destroyed, providing proof gets harder. Insurance companies know this and sometimes use it against you. That’s why documentation from before the fire—photos, videos, receipts—is gold. But even if you don’t have that, don’t worry. There’s ways around this problem, which is where professional help comes in.

| Item Category | Standard Policy Limit | Actual Value Could Be |

|---|---|---|

| Jewelry | $1,500 total | $10,000+ |

| Fine Art | $2,000 total | $25,000+ |

| Collections | $2,500 total | $20,000+ |

| Electronics | Per item limits apply | Varies |

| Cash/Currency | $200-500 | Varies |

The difference between handling your claim alone versus having a professional fire insurance adjuster can be tens or even hundreds of thousands of dollars. That ain’t exaggeration—it’s what we see every day.

Let’s be clear about something—the adjuster sent by your insurance company works for them, not for you. Their job is to close claims fast and pay out as little as possible. That ain’t evil, it’s just business. They got shareholders to answer to.

A public adjuster like us works only for you. We represent your interests, period. And we get paid as a percentage of what we recover for you—usually between 5-10% in Delaware. That means we don’t make money unless you do, and the more we get for you, the more we make too. Our interests line up perfectly with yours.

The numbers don’t lie. A study from the Office of Program Policy Analysis and Government Accountability found that people with public adjusters got settlements 574% higher than those without. That’s not a typo—over five times more money. Even after our fee, you come out way ahead.

Comparison of adjuster types:

When you hire us, we start with a free fire claim consultation. We’ll look at your policy, assess your situation, and give you our honest opinion about what we can do for you. Not every claim needs our help, and we’ll tell you straight if that’s the case. To schedule your consultation, call 302-279-2536 or email [email protected].

For total fire losses, we help with the overwhelming task of creating a complete inventory. We know what questions to ask to jog your memory, what categories insurance companies expect to see, and how to value items correctly. We got software specially designed for this.

Then comes the negotiation. This is where experience with Delaware insurance companies really matters. We know their tactics, their internal processes, and what arguments work with which companies. We speak their language and understand the fine print they try to use against you.

We handle all communication with the insurance company. No more frustrating phone calls where you’re put on hold forever or talk to someone new each time. We become your shield and your voice.

Our process timeline:

Learn more about our fire claim adjustment process for handling fire claims.

Take the Johnson family from New Castle County. Lightning struck their home during a summer storm last year, and the fire destroyed everything. The insurance company’s first offer was $380,000. They called us for a second opinion, and we immediately spotted problems with how the company calculated building costs and personal property values.

After we took over, their final settlement was $672,000—almost $300,000 more. That difference meant they could rebuild a home similar to what they had before instead of downsizing or taking on debt.

The timeline is important to understand too. Most total loss claims take 6-12 months to settle completely. If you’re fighting the insurance company yourself, it often takes longer. With professional representation, we can sometimes speed things up because we know how to prevent the delays insurance companies use to wear you down.

Read more fire claim success stories to see how we’ve helped other families.

Getting a fair settlement is just part of the journey. Rebuilding your life after losing everything in a fire is a long road that goes beyond money.

The emotional impact of losing your home can hit harder than people expect. It’s normal to feel grief, anger, and loss—you’re mourning not just things, but memories and your sense of safety.

Delaware has several support groups specifically for people who lost homes. The Delaware Psychological Association can connect you with counselors who specialize in trauma and loss. Many offer sliding scale fees, and some insurance policies actually cover mental health services after a disaster.

Children often struggle in different ways than adults. They may become anxious, have trouble sleeping, or regress in behavior. Delaware schools have counselors trained to help kids cope with major life disruptions like home fires. Don’t hesitate to talk to your child’s school about what happened.

Creating new memories and traditions helps the healing process. One family I worked with in Sussex County made a point of starting fresh traditions in their new home—a special dinner on the anniversary of moving in, a new holiday tradition. These new memories don’t replace what was lost, but they help you move forward.

If you need immediate advice after a fire, the Red Cross can provide emergency assistance, and the Federal Emergency Management Agency may offer additional support for larger disasters.

Picking the right people to rebuild your home is critical. Delaware has specific licensing requirements for contractors, but that don’t mean all licensed contractors are equal.

Check reviews carefully, ask for references from other fire rebuilds specifically, and verify insurance. The Delaware Division of Professional Regulation lets you verify licenses online. Beware of contractors who show up right after a fire offering immediate help—some target disaster victims for scams.

There’s actually some silver linings in rebuilding. Current building codes mean your new home will be more energy efficient, often with better materials than were available when your home was first built. Many clients end up with lower utility bills and maintenance costs in their new homes.

Managing a rebuild while living somewhere else is challenging. Set up regular site meetings, use project management apps to track progress, and keep communication channels open. Good contractors understand you’re not just a client—you’re someone trying to get their life back.

Contractor red flags to watch for:

There’s tax implications you need to know about. Generally, insurance proceeds for your primary residence aren’t taxable in Delaware, but there are exceptions. If you receive more than your tax basis in the property, you might owe taxes on that excess. Always consult with a tax professional about your specific situation.

If your insurance settlement isn’t enough, there are other financial options. The Small Business Administration offers disaster loans to homeowners, not just businesses. These loans often have lower interest rates than conventional loans. Delaware also has specific programs through the Delaware State Housing Authority that can help bridge funding gaps.

For tax-related questions after a disaster, call our office and we can connect you with tax professionals familiar with post-disaster situations.

Long-term financial planning is important too. Some people use a fire as a chance to reassess their housing needs. If your kids moved out years ago, maybe you don’t need to rebuild the same size house. Or maybe this is a chance to relocate to another part of Delaware that better suits your current lifestyle.

For more information about how we handle residential fire insurance claims, visit our dedicated page.

Losing your home to fire is one of the most difficult experiences anyone can face. But you don’t have to face it alone.

Delaware fire claims adjusters bring expertise, advocacy, and support when you need it most. The free fire claim consultation is free and creates no obligation. We’ll review your situation, explain your options, and let you decide if professional representation makes sense for your claim.

The sooner you reach out after a fire, the more we can help. Those early decisions matter tremendously in the final outcome of your claim. Don’t wait – call us now at 302-279-2536.

Remember—the insurance company has professionals working for their interests. Shouldn’t you have professionals working for yours?

Contact us for fire claim help today to schedule your free consultation. We serve all Delaware communities, from Wilmington to Rehoboth Beach, Dover to Newark, and everywhere in between. Your road to recovery starts with a single step.

CALL NOW: 302-279-2536

EMAIL: [email protected]

Have questions? Check out our comprehensive fire claim guide or call us directly at 302-279-2536.

Visit our main website to learn more about all the services we offer to homeowners dealing with insurance claims.

Do not hesitate to contact us. We’re a team of experts ready to talk to you.

© Copyright 2025 – Fire Claim Adjusters